Types of costs

Costs are usually classified according to their relationship with the level of output of the firm.

In practice, a firm will have three types of cost viz:

- Variable Cost

- Fixed Cost

- Semi-variable cost

Fixed costs

Fixed costs are costs that do not vary with the level of output in the short term.

Fixed costs stay the same month to month. They aren’t affected by your production volume or sales volume.

You can think of them as the price of staying in business: Even if your company isn’t making any sale, you have to pay your fixed costs. For instance, no matter how many rubber ducks you sell, your bathtub accessories store still needs to pay rent. And no matter how many clients your home-based acupuncture clinic attracts, you still need to pay property taxes.

Fixed costs appear on your income statement and balance sheet, but they tend to stay the same month to month.

Examples of fixed costs

- Rent

- Office salaries

- Advertising

- Insurance

- Depreciation

A common mistake made by candidates in examinations is to state that fixed costs will always remain constant. This is not the case, as these costs are fixed with respect to short-term changes in the level of output only. In the long-term, a firm may rent a second factory or take out more insurance cover, so fixed costs are likely to change.

Fixed costs can be represented on a graph and this would appear as follows:

source:intelligenteconomist

Variable costs

A variable cost varies in direct proportion with the level of output. Varying directly means that the total variable cost will be totally dependent on the level of output. If output doubles, then the variable cost would double. If halved, the variable costs would halve. If output were zero, then no variable costs would be incurred.

Common examples of variable costs are as follows:

Example of variable costs

- Direct labour

- Raw materials and components

- Packaging costs

- Royalties

Variable costs can be represented on a graph and this would appear as follows:

source:intelligenteconomist

the key difference between fixed and variable costs:

| Definition | Costs that vary/change depending on the company’s production volume | Costs that do not change in relation to production volume |

| When Production Increases | Total variable costs increase | Total fixed cost stays the same |

| When Production Decreases | Total variable costs decrease | Total fixed cost stays the same |

| Examples | Direct Materials (i.e. kilograms of wood, tons of cement) | Rent |

| Direct Labor (i.e. labor hours) | Advertising | |

| Insurance | ||

| Depreciation |

Semi-variable costs

A semi-variable cost is an expense, which includes a mixture of fixed and variable components. These costs vary (change) with output, but not in direct proportion The fixed cost element is the part of the cost that must be paid irrespective of the level of activity. On the other hand the variable component of the cost is payable proportionate to the level of activity. These costs are sometimes called mixed costs. In some cases, costs may be fixed for a set level of production, becoming variable after that level is exceeded.

source:teamstudy

Other costs concepts:

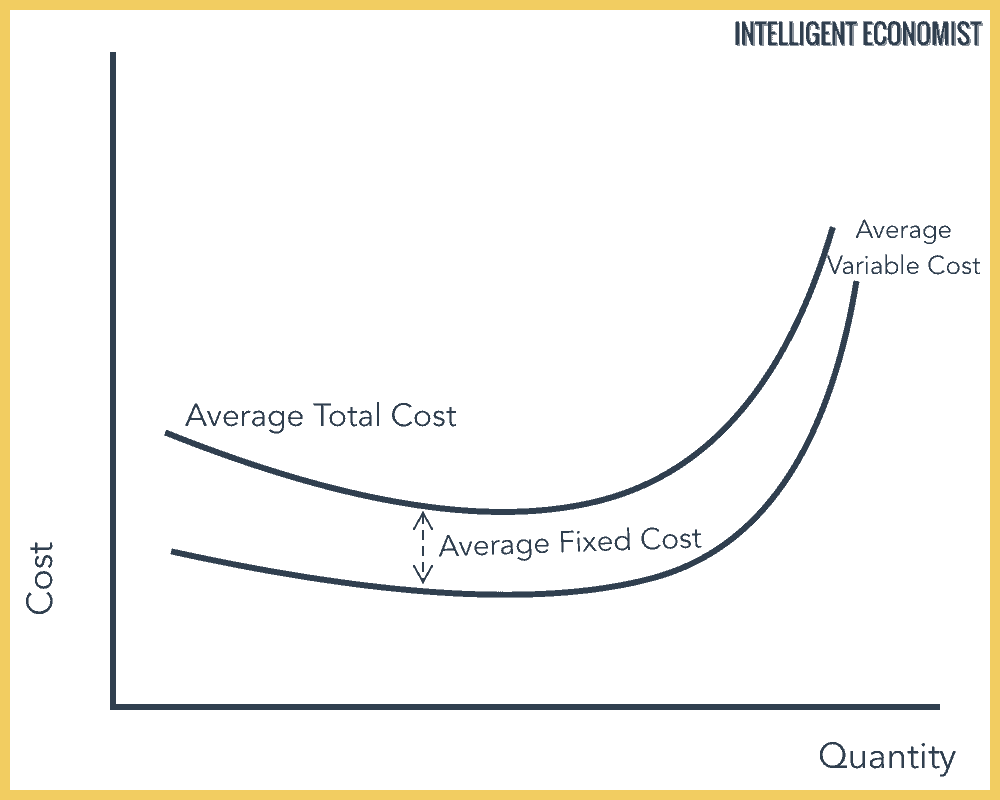

Average Fixed Cost

Average Fixed Cost = Fixed Costs/Quantity.

In the above diagram, we see that when the quantity produced is low, the average fixed cost is very high and this cost lowers as the quantity produced increases.

Marginal Cost

The marginal cost of production is the change in total production cost that comes from making or producing one additional unit. To calculate marginal cost, divide the change in production costs by the change in quantity.

Total cost

Total cost, the sum of all costs incurred by a firm in producing a certain level of output. It is typically expressed as the combination of all fixed costs (e.g., the costs of a building lease and of heavy machinery), which do not change with the quantity of output produced, and all variable costs (e.g., the costs of labour and of raw materials), which do change with the level of output.

Total Cost = Fixed Cost + Variable Cost