What is List Price?

List Price is the proposed retail price, which the manufacturer or distributor decides, and is listed in their catalog. The difference between the list price and the amount of discount is the net price.

Definition of Cash Discount

Cash Discount is a concession provided to the customers at a specified rate, for satisfying certain conditions of payment, primarily related to prompt cash settlement and also to avoid the credit risk. As the name suggests, cash discount is associated with cash flow, i.e. cash receipt or cash payment.

It encourages the buyer of the goods to make payment at the earliest in order to avail cash discount, and so he will have to pay a lesser sum, than the sum actually due to him. It is provided when the purchaser makes timely or early payment for the goods bought.

- Cash Discount recorded at the debit side of the cash book as discount allowed, whereas discount received appears at the credit side of the cash book.

- Such discount is allowed only when the customer makes payment of the debt within the stipulated time, i.e. prior to the expiry of the credit period.

- It is calculated on a percentage basis on the total amount payable by the customer.

For example, if an invoice is due in 30 days, a seller could offer the buyer a typical cash discount of 2% if they were to pay the invoice within the first 10 days of receiving it.

Small cash discounts benefit the seller because they increase the likelihood that a buyer will pay quickly. Cash discounts therefore provide the seller with cash faster; at times, it can be better to receive 95% of an invoice within a few days for example, rather than wait 30 or more days to receive the full amount.

Being paid early means that the seller can then reinvest the cash back into the business sooner.

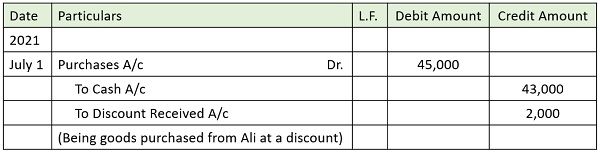

Example with Journal Entry

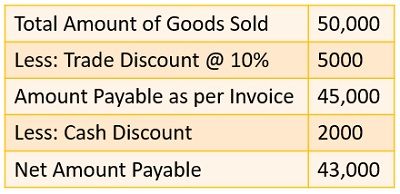

Suppose James purchased goods from Ali of the list price of Rs. 50,000, on July 1, 2021. Ali allowed a 10% discount to James on the list price, for purchasing goods in bulk quantity. Further, a discount of Rs. 2000 was allowed to him, for making the payment within 30 days.

So, first of all, the discount allowed on the list price of the goods, i.e. 10% of Rs. 50000 = Rs. 5000, is a trade discount, which is not going to be recorded in the books of accounts.

Next, the discount received by James of Rs. 2000 for making the quick payment is a cash discount, as it is allowed on the invoice price of the goods. A cash discount is entered in the books of accounts. Therefore, the journal entry for the transactions in the books of James is:

Journal Entry